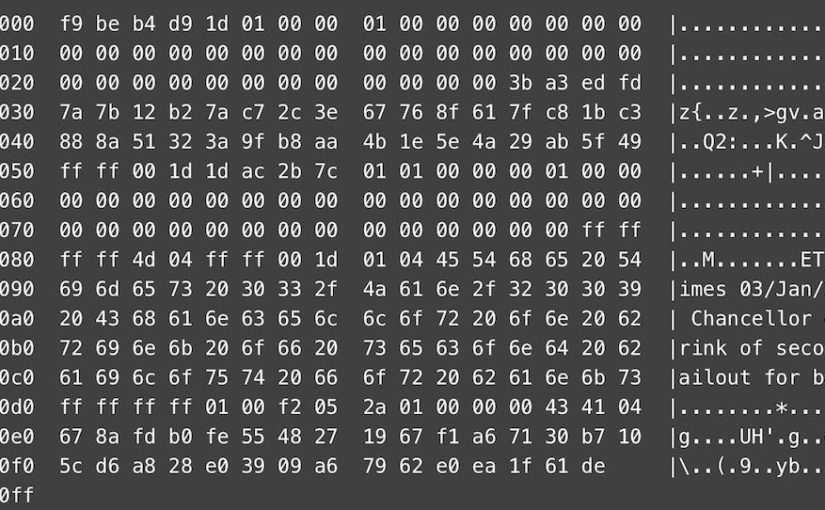

On this very day ten years ago – January 3, 2009 –, the Bitcoin network went live. Bitcoin’s first block, the Genesis Block, includes a short message as a reminder that the world was, at the time, finding itself in the midst of the biggest financial crisis since the 1920s. The message refers to the headline of the British newspaper “The Times” of that day:

“Chancellor on Brink of Second Bailout for Banks”

And, in fact, at about the same time as the Bitcoin whitepaper was published (October 31, 2008), the failure of Lehman Brothers as an issuer and underwriter of mortgage-backed securities initiated the largest insolvency proceedings in U.S. history and, subsequently, led to a major economic and political crisis of global dimensions.

Bitcoin’s inventor Satoshi Nakamoto is said to have picked that newspaper headline not only to create an immutable time reference for the genesis of the network but also to make a political statement (his own writings support the claim). As announced a few months prior to this event in the whitepaper, Bitcoin was intended to become a peer-to-peer electronic cash system, thereby eliminating the intermediating middleman – probably the prime source of fragility in today’s financial industry.

Cryptocurrency as money

Now, given the stated goal, the question is essentially whether Bitcoin and its numerous variants have since become what is commonly considered to be sound money. A recent analysis of Bitcoin as money can be found at Alt-M. In his short essay, the economist Larry White summarizes the state of the cryptocurrency as follows:

“Bitcoin should not be regarded as the last word in private money, but should be appreciated as a remarkable technological breakthrough. […] The inbuilt volatility of its purchasing power makes it unlikely to displace the incumbent fiat currencies barring an inflationary explosion.”

It is perhaps unsurprisingly, then, that people have begun to look into building stable coins based on blockchain technology. While there are already various – technically and legally – different types of stable coins, they often make a reference to a fiat currency, such as the US dollar or Swiss franc. In other words, they replicate their strengths and weaknesses: While most fiat currencies are exceptionally well-suited as transaction media, many of them are highly ineffective when it comes to storing value over time.

This is a real issue for poor people with very few or no options to diversify their savings.

Money and politics

The control over money is a powerful tool. That is why money and politics tend to go hand in hand. For slightly more than one hundred years, money has come into existence as fiat, i.e., unbacked currency created by an authority – typically the central bank of a country. Fiat currency might be managed diligently in the interest of the “greater good” (whatever that is supposed to mean). However, the past has been anything but a good track record of sound monetary policy. Therefore, it must have been inevitable for F.A. Hayek to refer to the history of money as an “all too monotonous and depressing […] story [of inflation]” (1976, p. 33-34).

Tokenization may be the answer!

Were it not for the efficiency of money as a medium of exchange, our economic system would revert to a simple barter and gift economy. However, modern monetary systems have become purely instrumental, entirely reduced to a means of creating money out of thin air. We can then ask ourselves: Why not rather link money to economic output than political influence, to real wealth instead of decreed purchasing power?

The implementation of this idea may be facilitated by tokenization:

Bitcoin and Ethereum involve native tokens. Such tokens are digital assets without any connection to real-world assets. Now, by means of tokenization, you can basically link tokens tradeable on the blockchain to any asset, in particular shares and bonds; such tokens that leverage the Bitcoin or Ethereum network as underlying platform are called asset-backed tokens.

Tradeability, however, is only the first step. The true nature of a good being money, as the economist Fritz Machlup put it, lies in its moneyness. “Moneyness” can best be defined as something, inter alia, durable, portable, fungible, and scarce. Furthermore, where a market exists, liquid trading of such good becomes viable.

Also, moneyness is a spectrum – some goods are better suited than others to be widely used as a medium of exchange. In other words, while some goods exhibit high degrees of moneyness – historically, this has been the case for precious metals such as gold and silver –, others only have modest levels of moneyness – services and bicycles are in a rather difficult position to gain widespread acceptance as a means of payment.

Tokenization of wealth

“But why use money to make transactions when computers offer the possibility to exchange goods and services for wealth?”

In his book “The End of Alchemy”, published in 2016, Mervyn King describes the transformation of the world of finance, the banking system, and money. The former Governor of the Bank of England, including during the period of the financial crisis, seems to envisage wealth being used as some sort of transaction medium.

What did he possibly mean by that?

As Swiss companies have recently begun to tokenize their stocks and bonds using blockchain technology, we will likely see in the future the emergence of freely tradeable and thus highly liquid stocks and bonds outside of traditional organized markets, such as a regulated stock exchange. To be fair: in most instances, such private offerings will unlikely succeed as a new means of payment, and, in many cases, this is not their intention anyway.

However, tokenization as a means to facilitate trade of shares and bonds on the blockchain, allows for a very simple solution that may eventually lead to a private means of payment.

How?

A company – let us call it “Private Money Ltd.” – that seeks to reflect the value creation in a given economy (e.g., the Swiss Gross Domestic Product, GDP) can purchase assets of the said economy, such as stocks, commodities, real estate, and company loans. By selecting good “proxy assets” for the underlying economy, Private Money Ltd. may effectively emulate the total economic output produced within a given country’s borders on its balance sheet. Now, holding shares of Private Money Ltd. would allow people to participate in the total wealth creation of a country as if they were purchasing each asset of the company’s balance sheet directly.

The company’s value would ideally grow or contract at the same speed as the economy’s GDP, thereby more or less keeping share price and production growth (or contraction) in balance. Keeping money stock and production growth (or slow-down) in balance is essentially the policy objective of central banks. However, a private company tokenizing its shares would be less prone to special public and private interests, yet still be accountable to their shareholders.

As mentioned above, since such shares would be tokenized, they would become easily accessible to everyone interested. The use of blockchain technology would allow for peer-to-peer exchange (P2P) as if the shares were regular banknotes and coins issued by a nation state. Given sufficient demand for the shares of Private Money Ltd., people could eventually start using them as a private means of exchange.

New forms of money on the horizon

Such a development may seem contrary to Bitcoin’s claim to be a P2P electronic cash system. Indeed, tokenization necessitates a certain degree of centralization. However, cryptocurrencies have, compared to a tokenized balance sheet, one great disadvantage, as they are not backed by anything other than computing power and people’s confidence in its hard coded safeguards. In other words, people typically have only poor expectations as regards Bitcoin’s “fair value”, resulting in a highly volatile price and purchasing power, respectively. A well-diversified asset portfolio is likely superior in terms of stabilizing market expectations in the long run.

Having said that, Bitcoin eventually evolving into money and asset-backed tokens being used as such need not be mutually exclusive.

No tokenization without Bitcoin!

In any case, there would be no tokenization without Bitcoin and Ethereum, no asset-backed tokens without their native predecessors. It is only thanks to Bitcoin’s ingenious monetary network design and Ethereum’s progress in developing sophisticated smart contract-systems that we are now able to talk about the likely emergence of new forms of money.

This is not the only reason (see, e.g., social scalability; censorship resistance and free speech; access to finance for the unbanked), but it is an important one for us to celebrate Bitcoin’s “genesis block” today.

Photo source: https://www.reddit.com/r/Bitcoin/comments/7ns2u7/nakamoto_remembers_the_times_03jan2009_chancellor/

Leave a Reply